Buddy Yates sits in the North Las Vegas home he has been fighting to keep out of foreclosure. The pastor, 60, fears his efforts will have been wasted if he doesn’t receive help.

Wednesday, Aug. 13, 2008 | 2 a.m.

Sun Topics

Sun Archives

- Home sales up for 7th month; prices fall (8-6-2008)

- Measuring population in moving boxes (8-4-2008)

- Nevada leads nation in rate of foreclosures (7-25-2008)

- Housing affordability seen as long-term problem (7-22-2008)

Buddy Yates sits at a dining room table awash in paperwork. The bills, late notices and letters represent his nearly yearlong quest to keep his family in the three-bedroom North Las Vegas tract home he bought two years ago.

In December, when he could no longer afford the $2,365-a-month payments, much less the higher payments set to kick in within months, he dialed up his Texas-based lender, EMC.

Yates, a 60-year-old pastor who officiates at valley wedding chapels, wanted the company to restructure his loan by lowering his payments and spreading them over a longer term.

By Yates’ account, he ran into a thicket of red tape.

After seemingly endless waits on hold, he told his story over and over because the same staffer wasn’t available. Company representatives would then give contradictory advice, he said.

“When you talk to some of those people it’s like talking to this table,” Yates said.

Despite lenders’ promises to step up efforts to work with homeowners facing foreclosure, about half won’t reach a deal with their bank, according to recent figures.

As of the second quarter of this year, 12,000 Nevada homes went into foreclosure. Lenders were in negotiations with just more than half that number, according to Hope Now, a nationwide mortgage industry group that offers foreclosure counseling.

But the number of borrowers in need of assistance is expected to grow.

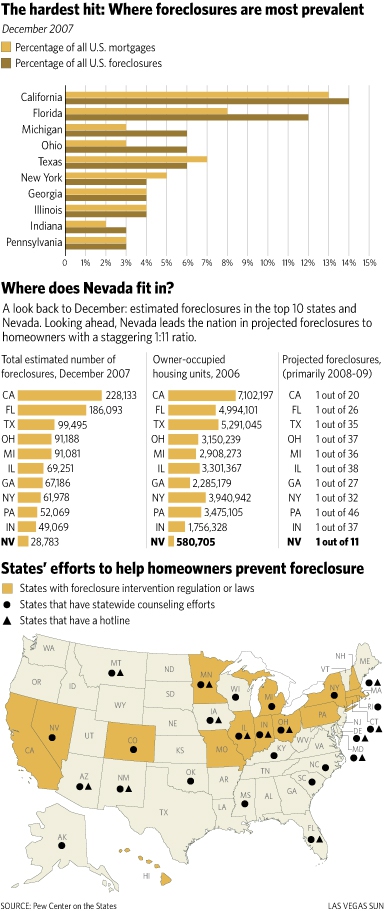

Nevada is expected to remain at the epicenter of the nation’s foreclosure crisis — the Pew Center on the States projects one in 11 homes in the state will enter foreclosure by 2010 — and Yates’ Sunrise Acres housing development seems to lie on a fault line.

Within one block of his home, more than a half-dozen residences are bank-owned or in some stage of the foreclosure process, according to Realty Trac, a Web site that maintains a nationwide database of foreclosed homes.

Like his neighbors, Yates was hit by a slumping economy and falling real estate values.

Last year, his income started to shrink as more couples skipped the trip to Las Vegas for their wedding and tied the knot at home. As it was getting harder for Yates to pay his $300,000 mortgage, the value of his home was dropping, and as a result he couldn’t refinance his loan.

Three weeks ago, Yates met his new neighbors, who had just purchased the house next door out of foreclosure for $167,000.

He figures his house isn’t worth much more. But it’s still home for him, his wife and their 4-year-old son.

Lenders have been deluged by borrowers seeking help.

“They just don’t have enough beating hearts to answer the phones,” said Kathleen Day at the Washington, D.C.-based Center for Responsible Lending.

Wells Fargo spokeswoman Natalie Brown said her company’s staff has grown fivefold to deal with delinquent loans than the bank had five years ago.

Debbie Krznarich of EMC, which holds Yates’ mortgage, would not discuss staffing levels at the company.

Even borrowers who reach their lender face obstacles.

Most loans have been sold to investors, who must approve deals with individual homeowners, Day said. Trustees who manage these loans are sometimes reluctant to modify them for fear of being sued by the investors.

What’s more, for borrowers who have second mortgages, both the first and second lien holders must agree to a deal before it can be offered to a homeowner.

Counselors who help troubled borrowers negotiate with their lenders are also swamped. Michelle Johnson, chief executive of Consumer Credit Counseling, reports that traffic at her agency is up 60 percent to 70 percent from last year.

Recent federal government initiatives to clean up the foreclosure mess have not helped Nevadans, Johnson said. An FHA program offers refinancing to homeowners with 3 percent equity in their homes, but few distressed homeowners in the state have any equity.

“The last I heard, there had not been a single (FHA refinance) loan made to anyone in Nevada,” she said.

The impact from the foreclosures extends beyond those who lose their homes.

The Pew Center predicts that in Nevada 77 percent of all homeowners, not just those in foreclosure, will feel the effects in the form of falling property values. That will have an impact on state and local tax revenue.

“It’s a concern for health, safety and economic viability,” said Lon DeWeese, chief financial officer of the Nevada Housing Division.

In June, Yates met face to face with an EMC representative.

EMC’s Krznarich said that Yates was offered a fair deal that would allow him to keep his home.

But Yates, who has missed more than one payment, said the repayment plan would put him only further behind. By the time he paid the arrears, he said, the interest rate on his adjustable-rate mortgage would go up, putting him back in the same predicament.

Yates has asked the Neighborhood Assistance Corporation of America, a nonprofit housing counseling group, for assistance. If he doesn’t get a reprieve, he said, he’s expecting a letter this month saying the company will foreclose on his home.

“When they sold you the home, they knew (with the adjustable interest rate), you weren’t going to be able to make the payment,” Yates said. “They don’t have compassion for the family who’s in the home.”

Explore Las Vegas’ past and present

Explore Las Vegas’ past and present Boomtown: The Story Behind Sin City

Boomtown: The Story Behind Sin City Neon Boneyard: A 360° look

Neon Boneyard: A 360° look Mob Ties: See the connections

Mob Ties: See the connections Implosions: Classic casinos crumble

Implosions: Classic casinos crumble

Join the Discussion:

Check this out for a full explanation of our conversion to the LiveFyre commenting system and instructions on how to sign up for an account.

Full comments policy